End of Content.

The AFMA MATRIX Magazine is a quarterly published magazine for our industry.

April - June 2026

Jan. - Mar. 2026

Oct. - Dec. 2025

April - June 2025

Oct. - Dec. 2024

Jul. - Sept. 2024

April - June 2024

Jan. - Mar. 2024

Oct. - Dec. 2023

Jul. - Sept. 2023

Apr. - June 2023

Vol 35 No 2 | April – June 2026

By Liesl Breytenbach, Executive Director, AFMA

Many of our members and industry stakeholders are operating in a consistently high-pressure environment. Disease management, evolving regulatory requirements, and broader economic uncertainty continue to test operational resilience across the value chain. Yet, this industry has demonstrated its ability not only to withstand disruption, but to adapt and move forward with purpose.

Encouragingly, positive production estimates for maize and oilseeds provide a measure of stability in terms of raw material availability. Improved crop prospects strengthen domestic supply fundamentals and offer welcome relief to procurement planning, providing a firmer foundation from which the industry can plan and operate with greater confidence.

Disease pressures

Among the most immediate pressures facing the livestock sector is the ongoing threat of animal disease outbreaks. We are operating in an environment where foot-and-mouth disease, African swine fever and avian influenza continue to place strain on South Africa’s livestock and animal protein value chain.

These outbreaks have had direct and measurable impacts on production systems, trade flows, and market stability. Each instance reinforces how interconnected our system truly is, from grain production to feed manufacturing, livestock production, processing, and ultimately the consumer’s plate.

When biosecurity measures tighten and markets respond, feed manufacturers remain a stabilising force. We must continue producing, maintain consistent quality, uphold regulatory compliance, and safeguard feed and food safety. AFMA’s role remains vital.

It is during times like these that the industry cannot afford division.

Disease outbreaks test alignment, trust, and collective responsibility. No single stakeholder can manage systemic risk alone; coordination, discipline, and unity across the value chain are essential. AFMA members are fully committed to prioritizing stringent biosecurity measures, traceability, and responsible sourcing within their operations. As an association, we will continue to promote responsible conduct and proactive risk management.

A more cohesive industry

AFMA recently convened another round of committee meetings, all held in person. Across five committees – technical, regulatory, trade, training and skills development, and marketing and promotion – we engaged directly with 113 member representatives. These sessions remain among the association’s most valuable engagements, ensuring that AFMA stays closely aligned with industry realities and responsive to the challenges facing our members. They also provide an important platform for members to exchange information and network with peers.

Regulatory progress

After many years of no significant updates to feed-specific regulations, the amended Farm Feed Regulations under the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act, 1947 (Act 36 of 1947) were published in January 2026 for public comment, marking the first major regulatory revision in over a decade.

Following extensive engagement with members across multiple committees, AFMA consolidated and formally submitted comprehensive industry inputs to the registrar’s office. We will continue to engage with authorities to ensure that the final framework supports feed safety and industry credibility while reducing unnecessary regulatory burden and remaining practical and workable for manufacturers. Implementation of the updated regulations is expected in June 2026.

AFMA Forum 2026

Preparations for AFMA Forum 2026 are well underway. The entire AFMA team is working with focus and purpose to create a platform where the industry can come together, engage, and reflect on the future of feed manufacturing. The theme, “The feed factor – the chain that feeds a nation”, reflects a simple but powerful reality that without feed, there is no livestock production; without livestock production, there is no animal protein; and without animal protein, there is no food security.

The AFMA Forum will be a strategic space designed to challenge conventional thinking, encourage robust dialogue, and inspire new perspectives. Our objective is clear: that every delegate leaves knowing they were part of a pivotal industry moment, one where ideas were tested, assumptions were challenged, and the future direction of our sector was thoughtfully shaped.

Looking ahead

In this edition of the AFMA Matrix, we continue to broaden the conversation beyond feed manufacturing alone. We include articles dedicated to industry issues – the competitiveness of the South African poultry industry, updates on animal health developments, and the latest progress in terms of the Agriculture and Agro Processing Master Plan, to name but a few. These contributions provide important insight into the broader industries we serve, and the structural and policy changes affecting their future.

I encourage all stakeholders to engage with these articles. Staying informed assists not only to anticipate change, but to lead through it. A sustainable feed industry depends on a resilient and competitive livestock sector.

By Bonita Cilliers, Techninal and Regulatory Advisor, AFMA

The footprint of every litre of milk, tray of eggs, and kilogram of meat produced in South Africa is made long before it reaches the farm gate or supermarket shelf. It starts with one essential input: animal feed.

Feed sits at the very beginning of the food production chain. Its quality and nutritional value affects animal health, farm productivity, and ultimately the safety of the food that reaches consumers. Scientifically formulated and responsibly manufactured feed supports efficient livestock production and helps ensure that farmers can produce safe, reliable food for the country.

Because of this central role, the South African feed industry operates within a regulatory framework governed by the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act, 1947 (Act 36 of 1947). Together with its associated regulations, this framework governs the registration, manufacture, importation, distribution, sale, and advertising of feed products. It sets clear standards, promotes fair competition, and protects farmers from misleading or substandard products.

In January this year, the Farm Feed Regulations were amended and published for public comment, representing the first major revision in nearly two decades. The amendments consolidate four existing farm feed regulations and introduce several updates that align with the latest feed technologies and feed safety measures; it also reduces unnecessary administrative burdens in product registration.

Why the change?

The animal feed industry has evolved over the last two decades. Modern livestock production relies heavily on specialised ingredients, advanced nutritional science, and sophisticated quality management systems. Moreover, global and local demands for traceability, antimicrobial stewardship, and transparency in food production have grown rapidly. Updating the regulatory framework was therefore necessary to align feed sector rules with modern production practices and scientific knowledge.

Key updates introduced in the amended regulations:

AFMA coordinated industry’s inputs throughout the consultation process, focussing on issues that will influence compliance, feed safety, enforcement, and fostering of an enabling environment for feed manufacturing.

Definitions and terminology

The amended regulations introduce several updates to the definitions that modernise regulatory terminology, broaden the scope of certain regulated products, and introduce several concepts that were previously applied in practice but not explicitly defined in legislation.

One notable change is the redefinition of ‘additives’ as ‘feed additives’. This expanded definition now includes micro-organisms, nutraceutical- type products, preparations, and certain herbal supplements, acknowledging that these substances may be administered through feed or drinking water. These updates reflect advances in modern animal nutrition and the growing importance of functional nutrition in livestock production, thereby bringing a wider range of products within the regulatory framework.

A stronger focus on feed safety and risk management is also evident, with definitions that have been introduced for carry-over, undesirable substances, restricted substances, withdrawal periods, and hazard analysis critical control points (HACCPs), supporting the legal basis for managing contamination risks and cross- contamination in feed manufacturing.

References to recognized laboratory accreditation systems such as SANAS and ILAC have also been incorporated.

Terminology relating to product registrations has been added, including amendments, minor administrative amendments, as well as parallel and daughter registrations. The definitions also clarify the difference between a feedstuff and an ingredient, aligning regulatory language with modern feed formulation practices.

For most stakeholders, these changes to definitions will not alter day-to-day operations, but will provide a stronger regulatory foundation and reduce uncertainty in the application of feed legislation.

Registrations and amendments

A major improvement is the introduction of a notification process for minor administrative amendments. Previously, even routine updates required full amendment applications, creating unnecessary delays and administrative burden. The new process reduces this constraint and allows technical advisors to focus exclusively on technical amendments that require assessment and may affect the composition, safety, or efficacy of a feed product.

Examples of minor administrative amendments include packaging artwork changes, additional pack sizes, removal of claims or pictorial elements, addition or removal of foreign language text, changes to registration holder address and contact details, and voluntary cancellation of a registration.

The regulations also recognize parallel and daughter registrations:

Professional accountability

The new regulations expand the allowance for professional accountability in declarations of nutritional adequacy for pet food. Such a declaration confirms that a feed/food product is formulated with appropriate ingredients and nutrient levels for the intended species, age, and stage, and that it complies with requirements regarding prohibited substances, undesirable substances, and unintended adverse effects relating to the specific mixture of feed/food ingredients and feeding recommendations of the product.

Previously, both farm feeds and pet food required validation by a professional animal scientist registered under the Natural Scientific Professions Act, 200 (Act 27 of 2003). Under the new regulations complete and complementary pet food may be submitted with a declaration signed by a veterinarian, while nutraceuticals and supplementary pet food may be signed off by a pharmacist. Both veterinarians and pharmacists must demonstrate appropriate expertise and experience in animal feed. Recognized international equivalents of these professionals are also accepted under the new regulations.

Professionally registered animal scientists will continue to be responsible for nutritional adequacy declarations for all farm feeds. AFMA notes the new allowance for pet food and cautions that it places an additional burden on the Act 36 technical advisor, who is professionally registered at SACNASP, to ensure that all pet food entering the market is nutritionally adequate, safe, and has the correct feeding recommendations on the label.

Updated feed classes

Continuous advances in animal nutrition technology have rendered many nutrient specifications and guaranteed analyses outdated.

AFMA has collaborated with the office of the Registrar of Act 36 over the past few years to review and update all livestock and poultry feed in line with the latest scientific developments as per the National Research Council (NRC). Reference sources were documented, and maximum tolerable levels (MTLs) for certain nutrients and substances were revised according to global best practice. The incorporation of updated nutritional specification tables and guaranteed analysis requirements into the Farm Feed General Guidelines is still pending.

A major new development is the addition of nutritional standards for game, which can now be regulated in South Africa for the first time. AFMA convened experts in game nutrition and after extensive research and discussions, submitted a recommendation to the Registrar for classification and nutrient specifications. This recommendation was adopted and is now included as a recognized animal feed type in the new regulations.

Other feed classes and types – such as complete, complementary and supplementary feeds, concentrates, as well as production-stage categories (pre-starter, starter, grower, finisher, post-finisher, weaning, and maintenance feeds) – have also been updated.

These revisions enable manufacturers to incorporate the latest feed technologies into formulations without requiring additional substantiation, ensuring alignment with international standards.

More practical labelling rules

The amended regulations also introduce improvements to feed labelling – date marking is now mandatory on all feed products. While AFMA members have already been voluntarily including date marks under the AFMA Code of Conduct, the new regulations make this practice compulsory across the market.

AFMA has, however, submitted a recommendation to the Registrar for a correction to the proposed date marking in the proposed regulations that will more accurately reflect a mechanism for the customer to evaluate the efficacy and safety of the animal feed product.

The proposed regulation amendment currently refers to ‘expiry date’ or ‘use-by date’, terminology typically associated with food safety risks in perishable products. Therefore, applying these terms to most animal feed may create confusion, as the majority of feeds and shelf-stable pet food are quality-stable products rather than safety-limited products. In practice, most feeds do not suddenly become unsafe after a specific date. Instead, product quality and certain nutritional characteristics may gradually decline depending on storage conditions.

AFMA therefore recommended the use of the following terms on feed product labels to support a risk-based approach and avoid misleading the customer into believing that stable feeds automatically become unsafe after a stated date:

The amended regulations also provide greater flexibility in label layout. Mandatory information no longer needs to appear in a fixed sequence, allowing manufacturers more flexibility in label design while ensuring required information remains clearly presented.

Practical approach to advertising

Previously, advertisements had to be approved by the Registrar before products could be marketed. This created delays particularly when approval backlogs occurred, making it difficult for manufacturers to promptly communicate product information or market innovations. The amended regulations now allow for a post-market compliance approach where advertisements no longer require prior approval. All advertisements must, however:

Advertising of unregistered feed products is explicitly prohibited. This change removes a significant administrative bottleneck while maintaining safeguards against misleading marketing.

Feed safety and traceability

The amended regulations place greater emphasis on feed safety systems, traceability, and recall readiness.

Manufacturers must ensure that facilities are suitable for feed production and may be required to demonstrate compliance with recognized quality or feed safety management systems. This typically includes good manufacturing practices for livestock feed and HACCP-based systems for pet food production.

Traceability and record-keeping requirements have been improved. Manufacturers must retain traceability records for at least five years and be able to demonstrate the ability to execute a product recall within four hours where necessary.

Updated provisions for reference sample retention have also been introduced. Reference samples must now be kept for the declared shelf life of the product plus one additional month, or until any product-related dispute has been resolved. Together, these measures reinforce the principle that feed safety should be managed proactively through structured quality systems, rather than relying solely on end-product testing.

Substance and carry-over risks The regulations introduce updated provisions for undesirable substances in feed. Several maximum allowable levels have been updated, including limits for heavy metals, mycotoxins, dioxins and pesticides, and now align closely with values used within the European Union regulatory framework. The unavoidable and unintended carry-over of veterinary medicine in feeds are being regulated in South Africa for the first time. Carry-over occurs when residual substances remain in manufacturing equipment and unintentionally enter subsequent feed batches. Manufacturers will have to demonstrate through verification that carry-over levels in untargeted feeds remain within permitted limits.

AFMA supports the inclusion of this regulation and provided the Registrar with science-based technical recommendations for establishing the required limits in the regulation. In December 2023 AFMA also published a Carry-over Code of Practice, providing practical guidance for feed manufacturers and premix producers on how to assess carry-over levels.

What happens next

The public comment period on the proposed amended regulations relating to farm feed closed in February this year and the Registrar is currently reviewing all comments submitted and drafting the final regulations for publication. Most provisions will come into effect six months after publication, allowing industry time to align labels, documentation and systems. However, Section 19 relating to controlled and undesirable substances takes effect immediately. It will be critical to update the Act 36 Farm Feed General Guidelines and Farm Feed Registration Guidelines and that it be published in conjunction with the final regulations. These documents are incorporated by reference in the regulation and provide guidance on the registration of products, formulation of feeds, and guaranteed analysis on labels. It is proposed that implementation is phased-in to prevent overflooding of the registration process due to label amendment requirements of the new regulation. AFMA will continue to collaborate with Act 36 and support the industry in ensuring a practical and reasonable implementation.

What the changes mean for industry

For feed manufacturers and suppliers, the amended regulations provide greater flexibility and use of technologically advanced products, improved definitions that contribute to greater regulatory clarity, and a more efficient registration process for minor administrative amendments and advertisements. For farmers and producers, the changes support improved product labelling and feed safety oversight. Ultimately, effective regulation supports more than compliance. It strengthens trust across the agricultural value chain and helps ensure that feed entering the market is safe, consistent, and fit for purpose. The AFMA Code of Conduct will be updated to reflect the new regulatory requirements and continue to provide a supportive self- regulating mechanism whereby industry can confirm compliance and provide customer assurance. Together, these measures strengthen the foundation of South Africa’s livestock value chain, from feed mill to farm to food production, and reinforce the principle that has guided the industry for decades: Safe feed for safe food.

By Petru Fourie, Operations Manager, AFMA

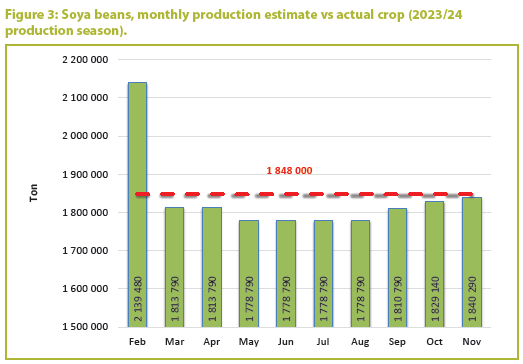

South Africa’s soya bean industry has undergone remarkable expansion over the past decade. Higher production volumes, supported by a bigger planting area and investment in local crushing capacity, have reduced South Africa’s reliance on imported soya bean products and improved raw material availability for feed manufacturers. Soya beans have also become South Africa’s second largest summer crop after maize, highlighting the rapid growth of the country’s oilseed sector. The area planted to soya beans has expanded from roughly 134 000ha in 2000 to more than 1,2 million ha today. This expansion, dryness that affected the yield potential. Nevertheless, overall production conditions remain favourable and continue to support a positive local soya bean supply outlook.

Supply-demand balance

South Africa’s soya bean market has become increasingly well supplied over the past three marketing seasons. Total supply for the 2026/27 marketing year is estimated at approximately 2,97 million tons, supported by good local production and higher carry-over stocks. One of the most notable developments in the market is the rise in ending stocks and soya beans available for export. Ending stocks are also projected to increase from around 140 000 tons in the 2024/25 marketing year to approximately 370 000 tons by the end of the 2026/27 marketing year (28 Feb 2027). Over the same period, soya bean exports are expected to increase from roughly 150 000 tons to 235 000 tons, reflecting greater soya bean availability in the local market and the growing role of exports in balancing supply. Local demand continues to be driven primarily by the crushing industry, with roughly 2,2 million tons of soya beans processed annually into oil and oilcake. This highlights the importance of the livestock feed sector as the primary downstream user of soya bean protein. Figure 1 illustrates the change in South Africa’s soya bean balance, with increasing exports and higher ending stocks indicating better supply conditions in recent marketing years.

Vol 35 No 1 | January – March 2026

By Liesl Breytenbach, Executive Director, AFMA

Each new year inevitably brings renewed energy and a sharpened sense of purpose. I trust that our members and industry partners have had the chance to rest and reconnect over the festive season. As we enter 2026, the feed industry finds itself at a defining moment. The Animal Feed Manufacturers Association (AFMA) will approach this year with clarity, resolve, and a firm conviction: The feed sector is not only adapting to change – it is shaping the future of South Africa’s agricultural and food value chain. AFMA Matrix has long served as AFMA’s voice: a bridge between science and industry, between policy decisions and practical implications. It is more than a publication – it is the sector’s narrative backbone. During 2025, AFMA refined the editorial direction of AFMA Matrix to ensure that each edition delivers targeted, sector-specific analysis that reflects the realities, opportunities, and innovations across South Africa’s feed-to food system. Members can expect even stronger insights from experts across trade, regulation, production, and infrastructure. Opportunity across the value chain. This first issue of 2026 reflects that renewed strategic intent to inform, connect, and inspire. It carries a central message for the feed and livestock industries: within challenges lie opportunities. After several difficult years, the poultry sector is demonstrating early signs of recovery. Continued improvements in disease control of highly pathogenic avian influenza (HPAI), biosecurity systems, and trade protection, underpinned by policy alignment, will be essential as phase two of the Poultry Masterplan advances. For the feed sector, this recovery reinforces the critical importance of efficiency, cost management, and innovation as drivers of national food security and competitiveness. Across the broader livestock value chain, cautious optimism is emerging. Softer feed prices, supported by higher soya bean production and stabilising market conditions, are creating space for improved performance, particularly in intensive production systems. Nonetheless, persistent challenges in disease management of foot-and mouth disease (FMD) and African swine fever (ASF), infrastructure reliability, and constrained consumer spending will influence the pace of growth. These are precisely the areas where the feed sector’s technical expertise from formulation to safety, quality assurance, and biosecurity continues to deliver tangible value.

Driving sustainable progress

As the industry evolves, attention must now shift decisively to the regulatory environment that governs agricultural inputs. The modernisation of the Fertilizers, Farm Feeds, Agricultural Remedies and Stock Remedies Act, 1947 (Act 36 of 1947) remains a priority area for collaboration between government and industry. The transition towards electronic submission systems, more effective oversight, and formal recognition of existing compliance initiatives across the feed and livestock sectors will collectively strengthen South Africa’s food production system. Logistics reform is equally pivotal. Rail and port performance continues to influence the reliability and affordability of feed ingredient supply. The revitalisation of Transnet and parallel logistics reforms will play a defining role in determining the sector’s growth trajectory over the coming years. Across all these themes, sustainability emerges as the unifying principle. Through engagement with the International Feed Industry Federation (IFIF) and Food an Agriculture Organization (FAO), AFMA has seen how global thinking has matured: Sustainability is no longer confined to environmental outcomes but extends to economic resilience, food safety, and social responsibility. For AFMA, sustainability is a practical, daily commitment ensuring that every tonne of feed produced contributes to a stronger, safer, and more efficient food system. Leading with purpose The articles in this issue underline a powerful reality, namely that the strength of the feed industry lies in its connectivity to primary producers, policy and regulation, trade and logistics systems, and global markets. It is an industry grounded in science, collaboration, and resilience, and one that continues to adapt to ensure South Africa’s agricultural future is competitive and secure. This year marks a new chapter for AFMA and the industry we serve. The challenges ahead require collaboration and innovation but they also offer a significant opportunity to reimagine the role of feed manufacturing in shaping a sustainable and inclusive food system for South Africa. AFMA’s vision for 2026 is to lead with purpose and to ensure our members are equipped with current information and the insights and confidence to act decisively. AFMA Matrix will continue to evolve as the industry’s trusted knowledge platform, reflecting both the technical depth and the forward-looking ambition that define our community. This year will undoubtedly bring challenges, but also unprecedented opportunity. Let’s meet them with courage and collaboration, knowing that our collective efforts strengthen not only the feed industry, but the broader food system that nourishes the nation.

By Susan Marais, Plaas Media

Wiana Louw is a stalwart in the South African grain value chain. From seed to feed, it would be difficult to find any segment untouched by her influence.

Although she will retire as general manager of the Southern African Grain Laboratory (SAGL) at the end of September this year, Wiana has no intention of settling into a typical pensioner’s life. In fact, simply writing these words feels as absurd to me as it will to anyone who knows her! Instead, she sees retirement as a launchpad for renewed innovation. As we sit in her office, sipping coffee, this becomes unmistakably clear. Wiana still speaks about her work with the enthusiasm of an eager intern discovering a world of possibilities – yet she carries the wisdom that comes only from decades spent at the coalface. Doing the best with the best. Over nearly 17 years at the SAGL, Wiana has witnessed remarkable developments and collaborated with exceptional people. “I have been very privileged to work with some of the best in the industry during the peak of their careers,” she says, adding that the role is any scientist’s dream because the SAGL is the link between academia and real world application. The laboratory’s work has also provided researchers with ample opportunities to advance their own careers through meaningful, industry benefitting research. One example is the PhD study by researcher Theresa de Beer, focussed on what has been dubbed ‘paprheology’. If the term is new to you, don’t worry – it was coined at the SAGL to describe this unique study. “Rheology refers to the study of dough quality, and Theresa is investigating the quality of pap, or cooked maize meal. So, we combined the two and came up with ‘paprheology’,” Wiana explains. “The rest of the world doesn’t cook and eat pap the way we do in Southern Africa, and people often underestimate how sophisticated our maize milling industry truly is. International visitors are always amazed when they encounter it.” Theresa’s research focusses specifically on methods to measure the stickiness of pap. It is also one of the reasons why Wiana wants to remain involved. Her scientific curiosity is far from satisfied. The vision continues The SAGL was born from the laboratories of the former Wheat and Maize Boards. In those early years, the laboratories performed basic tasks such as crop surveys and small-scale research for millers. Times have changed, however, and if Wiana has her way, they will continue to evolve. Her dream is for the laboratory to transform into a one-stop hub where every part of the industry can find answers to most, if not all, of their crop survey, grain measurement, and grain-related scientific questions. After all, scaling up is key to any laboratory’s longterm sustainability. “Many labs in other sectors are somewhat removed from the industries they serve. Yet we are right in the middle of the action, and it is wonderful to be here. It is great to truly be part of the value chain,” Wiana remarks. This proximity, she adds, gives the SAGL a unique advantage in understanding exactly what the industry aims to acheive.

One of the major issues Wiana hopes to focus on once she is ‘retired’ and has more time, is investing in people – both within the SAGL and across the broader industry. “People truly are your biggest asset, and it is critical for us to retain human capital as best as possible. To achieve this, we must ensure that our people feel safe and empowered.”To strengthen human-capital development even further, Wiana envisions helping to establish a training centre for grain monitoring and measurement scientists – a facility that could serve multiple industry bodies and companies beyond the SAGL. “There’s a lot of training happening across the grain and oilseed value chain, and there might even be room for consolidation.” Risk monitoring She also believes the SAGL may one day be well positioned to apply as an assignee of the Department of Agriculture. “If ever we are in such a position, I think it would be wise to start with a risk assessment of the industry and focus on the greatest risks first. You don’t have to be perfect from the outset, but you do need to start somewhere.” A potential starting point for monitoring risk in South Africa’s grain industry could be auditing the dry-matter content of bread. “Begin by reviewing companies’ records, identify gaps, and use that as your foundation,” she advises. Among her many career highlights is the establishment of the Crop Protection Division, which brought that part of the grain and oilseed value chain closer to the mainstream. Ultimately, there are countless research opportunities across the value chain that remain unexplored and Wiana believes the SAGL is ideally positioned to pursue them. Rooted in research Wiana is an educator at heart. She holds a Higher Education Diploma in Natural Sciences (now BSc Ed) from the University of the Free State, where she majored in botany, zoology, and chemistry. This academic foundation set the stage for her lifelong dedication to training, scientific rigour, and public health through food safety and regulatory compliance. Her professional journey began at Roodeplaat Research Laboratories (1988 to 1993) where she coordinated the National Residue Monitoring Programme. Her work centred on detecting pesticide and veterinary drug residues in animal derived products to ensure food safety and regulatory compliance. During this time, she played a key role in developing and validating analytical methods, as well as implementing quality management systems that led to achieving laboratory accreditation. She also demonstrated ethical leadership through her service on the institutional ethics committee. From 1993 to 1998, at the South African Bureau of Standards (SABS), Wiana continued her work in residue analysis, supporting product registration and monitoring. She was instrumental in securing ISO/IEC 17025 accreditation and OECD Good Laboratory Practice (GLP) compliance while mentoring new analysts and strengthening internal quality systems. Her tenure at the Council for Scientific and Industrial Research (CSIR) from 1998 to 2003 marked further expansion in pesticide and mycotoxin method development, and laboratory capacity building. She led cross functional projects and contributed to pharmaceutical research involving indigenous plant materials, effectively bridging traditional knowledge with contemporary scientific approaches. Wiana returned to the SABS from 2003 to 2009 to lead the Chromatographic Services Department. In this role, she oversaw pesticide and veterinary drug registration and residue monitoring activities, fortifying analytical capabilities and helping the agricultural sector meet both local and international standards. Wiana served at the SAGL from 2009, where she did some of her most impactful work. She established the National Mycotoxin Monitoring Programme, generating essential data to inform regulatory updates and underpin feed safety. The Crop Protection Division provides GLP-compliant services for plant protection product registration. Her contributions have extended into academia through support for tertiary institutions, internships, and pathways for postgraduate research and development.

Recognition and engagement Wiana’s contributions have been recognised through several accolades, notably her selection as a finalist in the 2017 Standard Bank Top Woman Awards and her nomination for the 2025 National Science and Technology Forum Management Award. Her influence spans a wide range of industry platforms. She serves on technical committees for agricultural trusts, the Animal Feed Manufacturers Association, Agbiz Grain, the National Chamber of Milling, and the South African Chamber of Baking. In these capacities, she has helped shape quality control systems and supported regulatory authorities through public-private partnerships that generate and interpret technical data for policy development. Wiana’s legacy is characterised by her unwavering commitment to innovation, capacity building, and regulatory excellence. Her leadership has elevated South Africa’s competitiveness in meeting international compliance standards, particularly in feed safety and analytical science. She has mentored numerous young scientists, championed skills development, and built strong collaborative bridges between academia and industry.

By Bonita Cilliers, technical and regulatory advisor, AFMA

Antimicrobial resistance (AMR) has become one of the defining global health and food security challenges of our era. Once hailed as the cornerstone of medical and veterinary progress, antimicrobials are losing their effectiveness as bacteria adapt and evolve faster than the development of new medicine. The scale of the crisis is staggering. According to the World Health Organization or WHO (2023), bacterial AMR was the direct cause of 1,27 million deaths in 2019 and contributed to almost five million additional deaths worldwide that same year. The World Bank warns that by 2030 AMR could cost the global economy up to US$3,4 trillion annually in lost productivity. Resistant pathogens move between people, animals, the environment and food, and demand a unified One Health response that connects human, animal, and environmental wellbeing. Under the leadership of the Quadripartite Alliance – comprising the Food and Agriculture Organization (FAO), World Organisation for Animal Health (WOAH), United Nations Environment Programme (UNEP), and WHO – the forthcoming Global Action Plan on AMR (2025 2035) calls for renewed global commitment to prevention, focussing on hospitals and the entire agri-food chain. Within this framework, the feed and livestock sectors play a decisive role. Preventing disease before it occurs through sound husbandry, biosecurity, and scientifically balanced nutrition is no longer optional; it is essential for safeguarding animal productivity, public health, and the long-term effectiveness of antimicrobials.

From use to stewardship

For more than 70 years, antimicrobials have supported livestock production by improving health, growth, and feed efficiency. When used responsibly and under veterinary guidance, they remain an indispensable tool for animal welfare and food safety. However, the misuse and overuse of these medicines, particularly at non therapeutic doses or without appropriate oversight, have contributed to the development and spread of AMR. The United States Food and Drug Administration’s Guidance for Industry no 72 (2023) and the WHO’s Critically Important Antimicrobials for Human Medicine (2022) both reinforce a central principle – stewardship, not prohibition. Medically important antimicrobials must be used only when necessary, under professional supervision, and for clearly defined therapeutic or preventive purposes. In animal nutrition, this stewardship mindset is rapidly gaining ground. The focus has shifted from dependency on antimicrobials towards holistic health, using high-quality feed, improved management, and nutritional innovation to reduce disease risk. The principle is clear: A healthy, well-fed animal is naturally more resilient and less reliant on antimicrobial intervention.

Global evidence

Research continues to map the uneven global burden of resistance. A study by Van Boeckel et al. (Science, 2019) identified AMR ‘hotspots’ across China, India, Pakistan, Brazil, Egypt, and Southern Africa – regions where livestock production is intensifying but feed quality and oversight remain inconsistent. Resistance to common antibiotics such as tetracyclines, sulphonamides, and penicillin already exceeds 40% in pigs and poultry in several of these regions. The findings underscore a simple but powerful truth: prevention must come before treatment. Vaccination, veterinary oversight, hygiene, and biosecurity remain indispensable, but nutrition has now been recognised as an equally vital pillar of prevention. The FAO, EFSA EMA (2017), and the Quadripartite Alliance all highlight that adequate animal nutrition improves gut health, immunity, and overall resilience, hence reducing the need for antimicrobials while maintaining productivity and welfare.

IFIF’s global leadership

Representing over Representing over 80% of global compound feed production, the International Feed Industry Federation (IFIF) has become a leading advocate for integrating nutrition into the global AMR response. Its flagship programme, Nutritional Innovation to Promote Animal Health and Welfare, provides a scientific and regulatory framework demonstrating how balanced feeding supports animal resilience and antimicrobial stewardship, particularly in low- and middle-income countries. The IFIF framework is built on three interlinked pillars:

• Scientific validation: Demonstrating measurable benefits of quality feed on gut integrity, immunity, and resilience.

• Regulatory clarity: Using the Delineation Approach (2023) to distinguish nutritional solutions from veterinary drugs and prevent over-regulation.

• Capacity building: Empowering national feed associations to advocate for nutrition as a recognised prevention tool.

Through collaboration with the FAO, WOAH, and Codex Alimentarius, IFIF ensures that advances in feed science are reflected in One Health dialogues, which bridge science and policy to promote preventive, sustainable animal health systems. Despite the growing evidence, regulatory recognition remains limited. The IFIF Regulatory Report (2020) notes that most national frameworks still treat feed mainly as a compositional or safety issue, while its health supporting functions often fall between veterinary and feed legislation. To close this gap, IFIF and the FAO recommend establishing harmonised criteria for nutritional health claims; recognising nutrition as an evidence-based resilience tool within AMR policy; and encouraging joint assessment mechanisms between feed and veterinary authorities.

Feeding for health

IFIF defines adequate nutrition as: “The oral intake by animals of adequate levels of nutrients, substances, microorganisms, and other feed constituents, considering their combination and presentation, necessary to fulfil functions related to their physiological states, including the expression of most normal behaviour, and their resilience capabilities to cope with stressors of various types encountered in appropriate husbandry conditions.” In practice, this means optimising feed composition, processing, and feed presentation; minimising exposure to feed borne contaminants such as mycotoxins; meeting nutritional needs for maintenance, growth, reproduction, and immunity; and supporting digestion, metabolism, and behavioural wellbeing. Adequate nutrition is therefore about feeding for health, not just growth, ensuring nutrient balance, gut integrity, and immune competence that create resilient animals less prone to disease and less dependent on antibiotics.

Nutrition as measurable prevention

Healthy, well-nourished animals are naturally more resilient to disease, respond better to vaccines, and recover from stress quicker. The EFSA EMA Joint Scientific Opinion (2017) outlines a threetiered prevention framework for reducing antimicrobial use in livestock, with nutrition as the foundation across all levels:

• Primary prevention stops pathogens from entering or spreading between farms through biosecurity, hygiene, and feed safety. Sound feed sourcing, mycotoxin control, and storage practices form the first line of defence.

• Secondary prevention reduces infection pressure via vaccination, housing design, and climate control, strengthened by balanced diet and probiotics that strengthen immunity.

• Tertiary prevention builds resilience and recovery through targeted nutritional support through functional feed additives such as enzymes, organic acids, pre- and probiotics, and trace minerals that improve gut health and immune function.

Across all tiers, nutrition is the unifying foundation for disease prevention, resilience, and reduced antimicrobial reliance. Evidence from IFIF recommendation papers (2019-2024) confirms that balanced nutrition measurably enhances gut integrity, immunity, and overall resilience.

Animal nutrition and AMR

The FAO (2024) brief Animal Nutrition Strategies and Options to Reduce the Use of Antimicrobials in Animal Production outlines key actions:

• Eliminate or minimise the use of antibiotic growth promoters, following Codex guidance.

• Adopt safe alternatives (enzymes, probiotics, prebiotics, organic acids, essential oils, and plant extracts).

• Improve husbandry and biosecurity, reducing stress, crowding and exposure.

• Apply good hygiene and feed safety practices across the value chain.

• Enhance welfare, water quality, and housing conditions.

• Avoid anti-nutritional factors (lectins, protease inhibitors) and optimise feed processing for digestibility.

• Build technical capacity through FAO/IFIF training and the Manual of Good Practices for the Feed Industry.

Together these steps shift production from antimicrobial dependence towards nutrition driven resilience and productivity.

Global alignment

AMR remains one of the highest priorities on both the global and national agendas. Following the 2024 UN GAP AMR declaration, South Africa reaffirmed its commitment to a One Health approach and the responsible use of antimicrobials across the food and animal production sectors. At the international level, the Quadripartite Alliance is finalising the Global Action Plan on AMR (2025- 2035). The plan promotes prevention, innovation, and capacity building as the foundation of global coordination, recognising animal nutrition as a key enabler of antimicrobial stewardship alongside vaccination, biosecurity, and responsible antimicrobial use. Its four priority areas include prevention through improved hygiene, vaccination, biosecurity, and balanced nutrition; innovation in vaccines, diagnostics, and nutritional strategies that strengthen resilience; capacity building and stronger governance, particularly in low- and middle-income countries; and surveillance and data integration to guide evidence based policymaking. Aligned with these global objectives, the FAO Guidelines on Animal Feeding reaffirm that good nutrition and sound husbandry are central to AMR prevention. They call for stronger feed governance, more research on immunity-enhancing feed additives, and the inclusion of nutritional indicators in AMR monitoring systems. As part of this global consultative process, AFMA participated as an observer in the GAP-AMR multi-stakeholder meetings in September 2025, ensuring that South Africa’s feed sector remains aligned with emerging One Health priorities and future international policy directions. As an active member of IFIF and participant in its regulatory committee, AFMA represents South Africa in global feed-policy discussions, ensuring national alignment with FAO-Codex guidance and international best practice. AFMA also promotes the recognition of adequate nutrition as a tertiary prevention measure within South Africa’s upcoming National AMR Action Plan, reinforcing the link between feed quality, animal health, and food safety.

National implementation

At a national level, South Africa is finalising its National AMR Action Plan for Veterinary Medicines, while the reconstitution of the ministerial advisory committee (MAC) on AMR is pending. Parallel regulatory reforms under the South African Health Products Regulatory Authority (SAHPRA) and the National Department of Agriculture (NDA) aim to enhance oversight, strengthen prudent-use practices, and antimicrobial stewardship across the value chain. Within this evolving policy environment, AFMA plays a pivotal role in bridging science and practice. As a member of the AMR Industry Alliance, AFMA ensures that feed safety, quality, and nutrition remain recognised as central pillars of antimicrobial stewardship. Its approach combines science based decision-making with practical implementation, recognising that safe, well formulated feed supports animal health and productivity. Building on this foundation, AFMA is supporting accurate antimicrobialusage reporting and contributing to evidence based decision-making before new restrictions are introduced; updating its position statement on antimicrobials to align with IFIF’s nutritional innovation framework, promoting ‘adequate nutrition’ as a science-based strategy to reduce antimicrobial reliance; and exploring the development of a standard operating procedure (SOP) on the prudent use of in-feed antimicrobials, guided by sector frameworks from poultry and swine.

Strengthening prevention

AFMA has elevated biosecurity as a cornerstone of disease prevention within the feed sector. Current initiatives include the distribution of the IFIF Biosecurity Guideline to members, development of a practical feedmill biosecurity audit checklist to support self-assessment and continuous improvement, and the publication of a SACNASP accredited CPD quiz to encourage learning and professional recognition of biosecurity competency. These initiatives – supported through the AFMA Code of Conduct and promoted across industry communication platforms – aim to strengthen on-farm and feed-mill controls, reduce disease risks, and enhance resilience at every level of production. By integrating biosecurity, feed safety, and nutrition as interconnected pillars, AFMA reinforces a comprehensive prevention model that supports animal health, food safety, and national food security.

Conclusion

Antimicrobial resistance is not a crisis of the future; it is a slow pandemic of today. Combating it requires prevention at the source – in feed, on farms, and across the food chain. Adequate nutrition, robust biosecurity, and responsible antimicrobial stewardship form the foundation of sustainable animal health. Through its collaborations with IFIF, the AMR Industry Alliance, and the Quadripartite AMR Platform, AFMA advocates science based, practical solutions that connect feed safety, biosecurity, and nutrition as the three pillars of prevention. By advancing evidence-driven policies, AFMA supports a national AMR response that safeguards public health while promoting animal welfare, sector sustainability, and national food security. By feeding for prevention, we build resilient animals, safer food, and a sustainable future – one where antimicrobials remain effective when truly needed.

Vol 34 No 4 | October – December 2025

By Anina Hunter, chairperson, AFMA

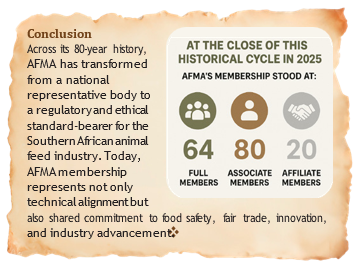

This year, the Animal Feed Manufacturers Association (AFMA) celebrates 80 years of growth, resilience, and service to the animal feed industry in South Africa. Since our establishment, AFMA has become a central force that unites stakeholders, advances industry practices, and drives food security as we stay true to our vision: To be a dynamic thought leader in animal feed, influencing food security through partnerships with all stakeholders, and ensuring ‘safe feed for safe food’.

With the global population projected to exceed nine billion by 2050, food production must increase by at least 60%. AFMA and its members have a critical role to play in meeting this demand and ensuring that animal proteins such as poultry, beef, and pork are produced a sustainable, affordable, and safe way, while maintaining consumer trust and regulatory compliance.

We continue to build a collaborative environment that brings together academia, regulators, and producers. This network promotes knowledge sharing and evidence-based solutions that help improve practices across the feed and livestock industries. In the past year, we have strengthened partnerships across the agricultural value chain, ensuring that AFMA remains the voice of our industry.

One of our notable contributions has been evaluating the impact of the soya meal import duty, which was introduced to support local soya bean cultivation and attract investment in crushing facilities.

From importing 80% of our needs, South Africa has now become self-sufficient in producing soya bean meal – a remarkable achievement that marks one of the greatest agricultural success stories of the past decade. As the industry reaches maturity, it is time to consider whether the duty has fulfilled its purpose.

AFMA plays a key role in coordinating disease prevention efforts. Outbreaks of African swine fever, foot-and-mouth disease, and avian influenza threaten livestock health, feed demand, and national food security. Biosecurity must

remain a top priority with support from government in terms of border protection, phytosanitary regulation, and vaccine approval. Notably, South Africa recently launched its first mass vaccination of poultry against avian influenza following an announcement and approval by the minister of agriculture, John Steenhuisen.

Competitiveness and operational efficiency continue to be challenged by port delays, road and rail deterioration, and utility disruptions. These infrastructure issues require urgent attention to safeguard the long-term viability of our sector.

AFMA recognises that today’s youth are tomorrow’s industry leaders. Through educational initiatives and student engagement programmes, we are investing in the next generation of agricultural professionals – ensuring that they are equipped with the knowledge, skills, and values required to lead with impact.

As we reflect on AFMA’s 80-year legacy, we reaffirm our commitment to leading the way forward. The animal feed sector will continue to play a central role in delivering safe, sustainable, and nutritious food for a growing global population.

Thank you to our members, partners, and the AFMA team for your continued commitment and dedication to this essential industry

By Petru Fourie, Operations Manager, AFMA

Over the past 80 years, the evolution of animal feed production in South Africa, as reflected through AFMA’s feedproduction, narrates a story of steady growth, technological innovation, and adapting market dynamics. Drawn from AFMA’s historical Chairman’s Reports and industry data, this article traces the development of feed manufacturing from its modest beginnings in the 1930’s to its current status as a multi-million-tonne industry, producing over seven million tonnes annually and shaping South Africa’s livestock and poultry production and food security.

The beginning: 1930s to 1950s

The South African animal feed industry took root during the economic hardships of the 1930s. Producers, grappling with droughts and limited resources, with a turnover of approximately £120 000. The installation of electrical feed mixers during this period laid the groundwork for compound feeds.

Post-war demand for animal protein and improved farming practices drove rapid growth. Halliday’s estimates show that production surged to 250 000t by 1945 and reached 450 000t by 1954. By the mid-1950s, the need for coordinated industry representation became clear.

The newly established Association of Balanced Feed Manufacturers, which would later evolve into AFMA, issued its first comprehensive report in 1956, describing the growth as “phenomenal”. That year, production was recorded at 621 000 tonnes, with turnover exceeding £10 million.

However, this expansion was not without setbacks. Feed production declined steadily, falling to 606 000t in 1957/58, 523 000t in 1958/59, and 497 000t in 1961/62. This contraction was attributed to favourable grazing seasons, increased on-farm mixing, and reduced demand for dairy and poultry feeds.

Recovery: 1960s to early 1970s

Feed production hovered at low levels for much of the early 1960s. AFMA Chairman’s Reports indicated that almost every raw material used in balanced feeds was in free supply, making home mixing increasingly attractive to producers. At the same time, declining egg export prices reduced the profitability of poultry producers, while surplus dairy products that could not be sold at economic prices limited the demand for commercial dairy feed. These factors, combined with producers relying on on-farm feed mixing, contributed to a prolonged slowdown in commercial feed production during this period.

Production only began to recover in the latter part of the decade. By the late 1960s, the industry began to recover as mechanisation of dairies and the intensification of poultry and pig production created new demand. Feed production nearly doubled from the 1960 low to 1970, marking the start of an unprecedented growth phase.

Surge and mid-1980s decline

The early 1980s brought renewed growth driven by severe drought conditions, which increased demand for beef and sheep feed. By 1981/82, production jumped to 3,24 million tonnes, one of the most significant increases in the industry’s history. However, this surge was short-lived. The economic recession of the mid-1980s, coupled with prolonged droughts and financial pressure on livestock producers, caused feed production to drop sharply.

By 1984/85, feed production fell to 2,88 million tonnes, and by 1985/86, to 2,73 million tonnes, the lowest levels since the early 1980s. This period also saw strong price competition as feed manufacturers could no longer use a single association- recommended price list. New competition laws required each company to set its own prices, leading to greater rivalry and lower profit margins.

Recovery resumed from 1986, with production increasing. The growth was driven primarily by beef and poultry feed production, although the industry remained under economic pressure.

Restructuring and stability: 1990s

The 1990s were a period of stabilisation and market restructuring. In 1989/90, feed production increased to 3,56 million tonnes, and by 1990/91 it reached 3,89 million tonnes, with poultry feeds making up 54% of the total. Despite this growth, AFMA’s reports noted that the commercial feed industry was still supplying only around 60% of the potential market, with significant volumes being home mixed. By the early 1990s, soya bean oilcake (mostly imported at the time) had become the primary protein source in feed formulations, replacing fishmeal due to its more stable supply and cost-effectiveness compared to the volatile fishmeal market.

Throughout the decade, production fluctuated between 3,6 and 3,9 million tonnes. By 1999/2000, AFMA members broke the four million tonne barrier, producing 4,12 million tonnes despite ongoing challenges in the poultry and dairy sectors.

Expansion: 2000s

The early 2000s saw steady growth supported by improved data collection and technological advancements in feed formulation. In 2007/08, AFMA recorded a historic milestone as production surpassed five million tonnes, reaching 5,16 million tonnes, a 10% year-on-year increase despite record-high raw material prices. Poultry, which had already become the largest feed category in the 1990s, strengthened its dominance during this decade, reflecting its central role in South Africa’s protein supply.

Technological growth: 2010s

The 2010s were marked by continued growth and industry modernisation. During this decade, AFMA established monthly feed production reporting, a step that greatly enhanced transparency, improved data-driven decision-making, and positioned the industry to respond more effectively to market shifts. Advances in genetics, feed efficiency, and data management further enhanced production. During this period, the growth in layer and breeder feeds also reflected consumer trends favouring eggs and value-added poultry products, reinforcing poultry’s role as the backbone of the industry.

By 2011/12, feed output reached 6,14 million tonnes, a record at the time. Despite challenges such as droughts, avian influenza outbreaks, and volatile global soya bean prices, the industry maintained a strong upward trajectory. The decade also saw the expansion of game feed production, driven by the growth of wildlife ranching.

Volatility and resilience: 2020s

The early 2020s were marked by market volatility but also showed the industry’s resilience. Production grew steadily and in 2022/23 broke through the seven million tonne mark for the first time, reaching a new record. This was followed by weaker demand, sectoral disruptions, and the severe impact of avian influenza, which led to widespread poultry culling and reduced feed usage. While earlier outbreaks in 2017 and 2021 had highlighted the industry’s vulnerability, the 2023/24 event had the most significant impact. By 2024/25, production recovered again to just over seven million tonnes, reflecting improved market conditions as the poultry sector stabilised.

Conclusion

From 12 000 tonnes in 1939 to the current seven million tonnes, the South African animal feed industry has undergone an extraordinary transformation. Its history is marked by cycles of expansion and contraction, shaped by market forces, climatic conditions, and regulatory shifts.

Through every challenge, AFMA’s coordinated efforts, data-driven strategies, and the industry’s ability to innovate have ensured its central role in supporting South Africa’s livestock and poultry sector.

By Petru Fourie, operations manager, AFMA

For much of the mid-20th century, fishmeal was the premium protein source in South Africa’s animal feed industry. With its exceptional digestibility, high lysine and methionine content, and consistent performance benefits, it became the cornerstone of starter diets for broilers, weaner pigs, and dairy calves. In certain high-performance poultry rations, inclusion rates even exceeded 10%, a clear sign of its value and the confidence the industry placed in it.

Over time, however, fishmeal’s dominance waned. Rising costs, inconsistent supply, and growing sustainability concerns opened the door for plant-based proteins such as soya bean and sunflower oilcake. This transition reshaped feed formulations and fundamentally shifted how the industry approached protein sourcing and long-term sustainability.

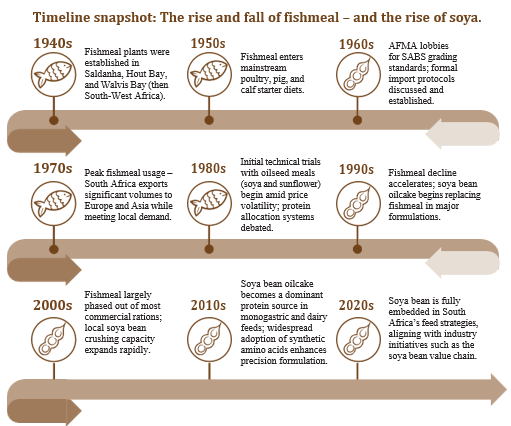

From by-product to protein (1940s to 1960s)

The commercial production of fishmeal in South Africa began in the 1940s, spurred by the growth of coastal fisheries along the West Coast. Offal from anchovy and pilchard processing, once discarded as waste, was transformed into high-protein meal at plants in Saldanha, Hout Bay, and Walvis Bay.

By the 1950s, fishmeal was considered the premium protein source. It boosted feed conversion ratios, supported rapid growth in young animals, and delivered consistency across rations. During this period, AFMA committees actively discussed fishmeal imports from South West Africa and Peru, while also raising early concerns about the need for standardised quality control protocols.

While fishmeal was celebrated for its nutritional excellence, even at this early stage concerns emerged: price volatility, seasonal availability, and quality inconsistencies foreshadowed future vulnerabilities.

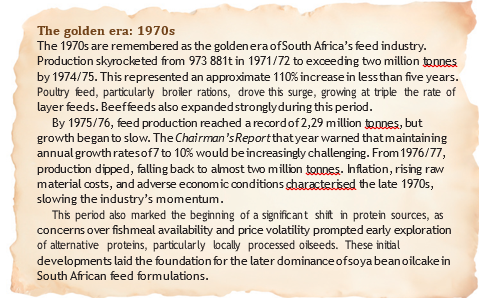

The height of fishmeal use (1970s to 1980s)

The 1970s ushered in the golden age of fishmeal in South Africa. During this period, the country exported fishmeal to Europe and Asia, while still meeting strong domestic demand. Poultry starter diets frequently included 10 to 12% fishmeal, and it featured prominently in rations for dairy calves and piglets. With domestic animal production booming, fishmeal was both affordable and abundant. It offered critical nutrients such as lysine, methionine, and calcium, vital in supporting early growth stages and reproductive performance.

Minutes from AFMA technical and executive committee meetings in the late 1970s repeatedly started to highlight member frustration over sudden fishmeal price surges and allocation inconsistencies, as export prioritisation during high-price cycles further tightened local supply.

Chairman’s Reports from this era frequently stressed the need for stricter quality standards and improved supply security.

During severe shortages between 1983 and 1984, AFMA even proposed establishing a fishmeal importation company to stabilise supply, highlighting the strategic importance of fishmeal at the time.

Shifting tides: The 1990s

By the 1990s, fishmeal’s dominance waned under mounting pressures: stricter environmental controls on processing plants, tighter marine quotas introduced later in the decade, and rising global competition from markets such as China and Europe.

AFMA members began reformulating broiler diets to reduce or exclude fishmeal, aided by synthetic amino acids that allowed plant proteins to match its performance. This shift paved the way for soya bean oilcake, supported by imports from Argentina and Brazil and the gradual expansion of local crushing capacity.

AFMA’s technical committees compared cost-performance models for oilcake- based diets, while tariff debates and calls for import rebates highlighted the need to secure affordable protein supplies.

Turnaround: 2000s to 2010s

The early 2000s marked a turning point for the feed industry, as aflatoxin contamination in groundnut oilcake heightened the need for safer, more consistent protein alternatives. Fishmeal, while still a high-quality ingredient, had become costly and its availability increasingly erratic due to global demand and marine resource constraints, discouraging its use in standard formulations.

By the 2010s, fishmeal’s role in mainstream commercial feed had fallen to trace levels, confined mainly to specialised applications, high-end pet foods, and select breeder rations that required top-tier nutrition. In contrast, soya bean oilcake rose rapidly, driven by local investments in crushing plants and supported by genetically modified (GMO) soya bean varieties that improved both supply stability and protein consistency.

Soya bean oilcake: More than a substitute

The rise of soya bean oilcake was not merely a response to fishmeal’s decline; it marked a structural shift in South Africa’s protein sourcing. Initially reliant on imports, the feed industry soon recognised the value of expanded domestic crushing capacity, which stabilised supply and reduced dependency on volatile imports. Combined with advances in synthetic amino acids and enzymes, soya bean oilcake became the cornerstone of modern feed formulations.

Legacy and lessons

The decline of fishmeal was more than an ingredient change; it forced the industry to innovate, diversify, and embrace sustainability. Synthetic amino acids allowed plant proteins to deliver performance on par with animal-derived ingredients. Today, soya bean oilcake is firmly entrenched as a foundational ingredient, not a fallback. Its rise reflects AFMA’s pivotal role in helping the feed industry navigate transitions while maintaining both nutritional performance and economic resilience.

Conclusion

What began as a discarded by-product of the fishing industry evolved into a pillar of animal nutrition, only to be overtaken by soya bean oilcake in a new era defined by precision and sustainability. From lobbying for quality standards to shaping trade discussions and supporting local value chain development, AFMA played a crucial part in this transformation.

As AFMA marks 80 years, the journey from ocean to oilcake stands as a testament to the industry’s innovation, collaboration, and resilience.

By Wimpie Groenewald, member liaison officer, AFMA

From its humble beginnings in the 1930s, marked by the installation of South Africa’s first five-tonne electric feed mixer, the country’s animal feed industry began its journey towards structured organisation and professionalisation.

In 1945, the establishment of the Association of Balanced Feed Manufacturers marked the industry’s first formal step towards collective representation. Two years later, in 1947, the Association hosted its first annual general meeting, setting the stage for what would later become the Animal Feed Manufacturers Association (AFMA), the recognised voice of Southern Africa’s feed industry.

Expansion and consolidation

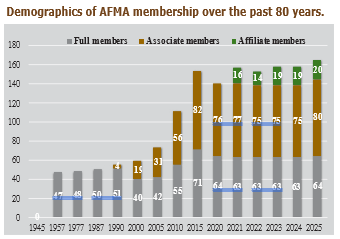

By 1956, AFMA’s predecessor had achieved significant growth, adding eight new members and approaching full representation of the national feed industry. By 1957, the Association had 47 full members covering approximately 99% of South Africa’s feed tonnage, a level of consolidation rare in the sector at the time. Membership remained stable through 1958.

However, the early 1960s saw fluctuating numbers. Membership fell to 30 full members in 1961, though associate membership was recorded for the first time. A shift towards industry-defined standards emerged in 1965, as the Association moved away from reliance on the SABS Bureau Mark, signalling the start of independent self-regulation.

In 1962, with the move to a more independent office space and a new membership fee structure (R10,50 per member plus a levy of ½ cent per tonne of feed), the organisation laid the groundwork for a more predictable revenue model and professionalised membership administration. This step allowed AFMA to expand its services and deepen its technical engagement, drawing more feed companies into the fold.

In 1976, rising member concerns regarding voting fairness and representation led to the formation of AFMA’s first constitutional subcommittee and costing standards committee – one of the Association’s earliest governance reforms.

By 1980, membership had rebounded strongly to 61 full members from 35 recorded a decade earlier. This growth was solidified in 1983 when AFMA reached 68 members, representing 94% of national feed sales.

A key development in the 1980s was the formalisation of associate membership, allowing suppliers, equipment providers, and non-manufacturing stakeholders to participate in the AFMA ecosystem. This diversification was important for broadening AFMA’s influence across the value chain.

Yet, by 1986, membership declined slightly to 50 full members, prompting structural and ethical reforms related to pricing practices, constitutional alignment, and emerging competition legislation.

Compliance and diversification

In the early 2000s, AFMA formalised its compliance framework, culminating in the 2006 registration of its ‘Safe Feed for Safe Food’ trademark. A major milestone followed in 2008 when compliance with the CoC became mandatory for all members. Meadow Feeds became the first full member to comply, followed by Ceva Animal Health as the first associate member in 2009.

These achievements underscored AFMA’s leadership in food safety and regulatory enforcement.

Between 2008 and 2015, the CoC evolved into AFMA’s core standard, supported by audit protocols, transport standards, and traceability systems.

This period also saw rapid membership growth, particularly among associate members (reaching 82 by 2015) as the organisation welcomed traders, service providers, and premix suppliers.

By 2011, AFMA had expanded its focus to include industry training and accreditation, offering members access to technical workshops, global symposiums, and formal feed miller qualifications, reinforcing its role as both a regulatory and professional development leader.

Regional leadership

By 2015, AFMA had extended its influence beyond South African borders, collaborating in the establishment of regional industry bodies such as the Southern Africa Feed Manufacturers Association (SAFMA) and the Tanzania Feed Manufacturers Association (TAFMA). This regional expansion was complemented by increased collaboration with agricultural and food safety institutions across Southern Africa.

In 2018, AFMA supported the formation of the Zambian Animal Feed Manufacturers Association (ZAFMA), modelled on AFMA’s governance principles. This initiative, along with mentorship of the Association Kenya Feed Manufacturers (AKEFEMA), further positioned AFMA as a leader in regional industry development.

Adaptation and structures

Despite pandemic-related disruptions in 2020, AFMA maintained regional engagements while innovating its compliance systems. By mid-2021, audits resumed, expanded to a 12-point system, and pre- screening phases were introduced to enhance audit rigor.

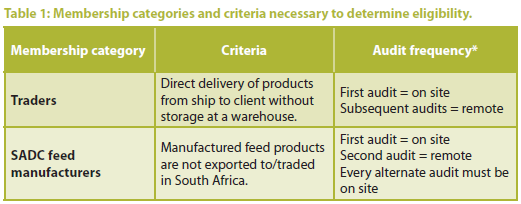

By 2025, AFMA had introduced remote audits for traders without warehousing and for manufacturers located in Southern African Development Community (SADC) countries not exporting into South Africa – a pragmatic step towards embracing modern inspection methods while expanding membership inclusivity.

During this time, AFMA also formalised warehouse audits and off-site storage inspections, ensuring all members upheld exacting standards of traceability and feed safety – regardless of their operational footprint

Since its founding, AFMA has championed the professionalisation and ethical development of the animal feed sector in Southern Africa. Central to this mission has been the creation of the AFMA Code of Conduct (CoC), a framework that has evolved from informal ethical agreements into one of the continent’s most robust, auditable self-regulatory systems.

As the industry matured, so too has the CoC, adapting to emerging risks, technological changes, and global standards. This article traces the remarkable journey of the CoC, showcasing how AFMA has institutionalised accountability while promoting trust, safety, and international alignment across the feed value chain.

Laying the groundwork

AFMA’s commitment to ethical practices began long before formal compliance systems were the norm. In the 1960s, then operating as the Association of Balanced Feed Manufacturers, AFMA spearheaded the push for the specifications of poultry feed under South African Bureau of Standards (SABS) standardisation and discouraged unregulated home-mixing.

A defining moment came in 1965 when members voluntarily withdrew from using the SABS bureau mark, signalling a collective confidence in self-regulation.

By the 1970s, industry concerns around pricing transparency and governance catalysed the formation of AFMA’s first constitutional and costing subcommittees. These laid the groundwork for modern compliance, establishing early systems of accountability and procedural integrity. In 1976 AFMA drafted its first Code of Practice (COP) for feed manufacturing, marking the beginning of formal self-regulation and a commitment to quality. The year 1981 earmarked the refinement of the draft COP into a more detailed framework covering production hygiene, ingredient integrity, and formulation practices.

Codification and formalisation

The 1990s marked the transition from ethical norms to formalised standards. In 1992, AFMA introduced its first internal CoC, targeting hygiene risks such as poultry litter in feed. Although unpublished, this set a critical precedent for future safety and hygiene benchmarks. That same year, AFMA launched AFMA Matrix, a quarterly publication that remains instrumental in disseminating best practices and compliance updates to this day.

A landmark achievement followed in 1994 with the adoption of a COP for Salmonella control, modelled after European Feed Manufacturers’ Federation guidelines. By 1996, the COP had formalised feed hygiene and risk management practices. Concurrently, AFMA began drafting a good manufacturing practices (GMP) code, shifting focus from product registration under Act 36 of 1947 to facility- level quality control. The draft, submitted to the Registrar in 1999, would become a precursor to today’s compliance framework.

Voluntary to mandatory compliance

The turn of the millennium ushered in a new era for AFMA. In 2004, the Board approved the development of a formal, auditable CoC. A year later, the first official draft was released, coinciding with rising global concern over feed safety, traceability, and consumer protection.

In 2006, AFMA registered its iconic slogan Safe Feed for Safe Food and by 2008, compliance with the CoC became mandatory for all members. This landmark policy shift marked the transition from voluntary ethics to enforceable standards. Independent audits were initiated through Afri Compliance, using a rigorous nine-point audit framework.

Meadow Feeds became the first full member to meet all requirements, with Ceva Animal Health following as the first associate member in 2009. This era also laid the groundwork for structured enforcement, membership accountability, and continuous improvement through third-party evaluation.

Regional integration

Between 2010 and 2025, AFMA’s CoC evolved into a mature, regionally recognised, and digitally enabled compliance system. The audit framework expanded to ten points in 2010, incorporating transport standards for biosecurity and traceability, and by 2014 most members had completed their third audit cycle. Regional recognition followed, with Meaders Feeds becoming the first Southern African Development Community (SADC)-compliant member in 2011 and AFMA collaborating with the Southern African Feed Manufacturers Association (SAFMA) and SADC initiatives by 2015.

From 2016 onward, AFMA assumed full responsibility for the audit process, rolling out the system in phased stages, boosting efficiency and transparency. The CoC inspired regional adoption, including the Zambian Animal Feed Manufacturers Association (ZAFMA) in 2018 and Association Kenya Feed Manufacturers (AKEFEMA) in 2020. After a brief Covid-19 pause, audits resumed in 2021 with a 12-point audit framework, pre-audit screening, and full in-house administration.

To strengthen oversight, AFMA introduced affiliate membership and warehouse audits in 2022 and, by 2025, remote audits for SADC-based traders and facilities. These innovations reflect a maturing, adaptable system that supports both local and regional feed industry accountability.

Modernising for the future

The CoC is now in Phase 3 of a major modernisation initiative. Focus areas include benchmarking the Code against the 2021 audit criteria, pilot testing, assessment body expansion, and implementation. One of AFMA’s most critical priorities is expanding the pool of accredited assessment bodies. While Afri Compliance remains the sole provider, various additional certification bodies currently used by members are under review. All providers will use a unified AFMA audit template to ensure consistent application across the board.

Certification benchmarking

A member survey conducted in early 2025 revealed that 57% of AFMA members – including 65% of associate members and 48% of full members – operate without formal certifications such as hazard analysis and critical control points (HACCP), GMP, or International Organization for Standardization (ISO). Instead, they rely exclusively on the AFMA CoC as their primary quality system.

To ensure global alignment while maintaining local practicality, the code was benchmarked across four dimensions:

Based on the findings, AFMA is in the process of revising the 2021 version of the CoC audit manual and audit sheets to ensure a fit-for-purpose model that balances rigour with applicability for South African operations.